Asset-based lending seems pretty easy, right?

On paper, it looks straightforward. Developing the agreements, specifying the collateral, conditions, monitoring, sign, “easy-peasy.” All seem pretty easy as many other parties are crafting the deal and hammering out the details, the so-called experts. But who watches your back, checking the experts ensuring the deal at stake will serve your company’s best interest, now and going forward, the company you have built over many years?.

It’s all very exciting. But wait….., until realities start to set in, the arrangement quickly can change from the sunny blue-sky mornings into a thunderous storm.

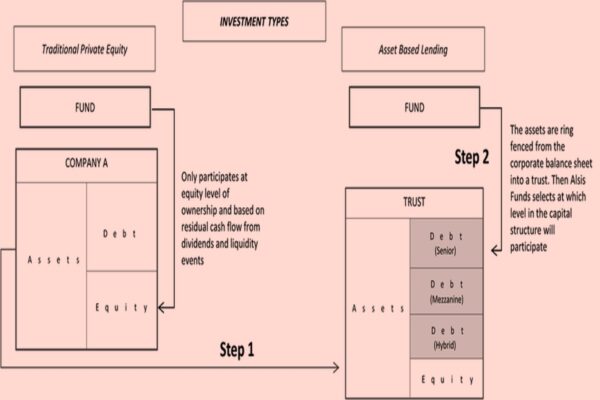

Know the pitfalls attached to asset-based lending. These pitfalls could destroy your business. Banks and some private equity investors provide Asset-based lending. It is not Receivables Factoring, nor is it Securitization. It is secured lending against the assets of the business. It’s a great form of finance to fund growth, or finance a turn-around strategy. Asset-based lending, whether from a bank or a private investment fund is expensive. For that reason it is paramount to ensure that notwithstanding having the future cash flow to repay and service the debt, that the covenant and conditions are supportive of the business and not impairing, or slowing growth.

Companies and businessess with weak, or negative operating cycles (the length of the Order-to-Cash cycle is LONGER than the length of the Procure-to-Pay cycle) run the risk of not benefiting from asset-based lending. In such a case, it is wise to first work-out the plans that can improve the operating cycle, or improve margins to ensure that the full productive benefits of asset-based lending advance the business.

The conditions and ongoing reporting requirements combined with collateral ineligibility pose the biggest challenge in managing the arrangement to benefit all, the funder and the company. If you are not proactive-operationally and reporting-wise set-up from the word “go”, be assured there are lots of pain down the road.

The pain intensifies, and your business is in a challenging financial position. Many factors can lead to financial distress. However, financial distress and asset-based lending don’t always jell so well. It could, if approached with the required guardrails to manage relational conflicts.

Lender anxiety can quickly turn your business into working 24/7 for the funder. The funder is becoming prescriptive and unreasonably demanding around every corner, daily. Watch out for “holding a proverbial gun against your head”, when things get tough with statements like, “we are writing the cheques around here, and you better do as we say” – that is so mafioso!. Such statements are about power posturing. The funders need you to protect and manage the business so that their collateral is crisp and remains valuable. We all get that; not hard to understand that.

In severe circumstances, funder expectations rocket off to the moon when in reality, the desired outcomes are best served with the approach to let everyone do the job they are good at. Will you tell a Cardiac Surgeon what to do during a ~4-hour triple bypass procedure? I don’t believe it will end well. Same here.

Respect the people inside the business and business owners to do what they are good at, taking the lender requirements into account. Sometimes it is as simple as developing a new process, modifying an existing process, or more importantly, allowing the required improvements to run their course to materialize the benefits that serve both parties very well. But for heaven’s sake, avoid letting too many cooks into your kitchen; it will quickly turn into a disaster that otherwise could be prevented. The meal is going to get spoiled, and the steaks will burn. Creating an extremely unpleasant situation for all. These situations will quickly drain the energy out of everyone, leaving the asset-based funder and your company in challenging positions.

That is a problem as it “steals” away valuable time to fix business and operational problems, implement and execute strategy, grow the business, valuable time needed by the finance team to make the required improvements.

Entrepreneurs don’t always relate well to these asset-based lending conditions as they focus on sales and growth. Asset-based lending conditions seem fine on paper, it’s straightforward to agree to them when in financial distress and the only viable likely outcome at that time. It’s easy to get swept away by the size of the funding package. But relax. It does not mean your company can access all those funds all at once. That’s where the status and performance of the collateral comes in.

Asset-based lending, notwithstanding benefiting from the collateral, price-in at high lending rates. In some instances cheaper than a traditional bank loan. Asset-based lending comes with juicy fees, including, in some cases, fees for the unused portion of the funding package amid tieing up capital for the funder that costs money. Sorry, that’s not the business owner’s cost of doing business. It places the business between a rock and a hard place. Extra funding may not be accessible due to the collateral status; thus, the un-drawn and the un-used portion of the funding package, given the collateral status, may not be accessible, and yet you are charged fees for that.

Entrepreneurs and business owners, beware, don’t sell your soul, or ensure that you have a strong internal team under your tent to help negotiate the conditions and implement the practical workings (emphasis added) to avoid disaster and frustration down the road. Asset-based lending should not be attempted without adult supervision of dedicated resources on your side (emphasis added).

I speak from extensive experience where things worked out extremely well for all parties through a negative pledge exchange-listed corporate bond collateral program to highly restrictive asset-based lending with vastly restrictive impairing requirements and conditions attached to it in managing the practicalities of the arrangement. The latter smothers effort, spirit, and morale.

If you are not careful, the post-deal, post-utopian era, after the champaign, the investment banking-AAA-Beef-Rib-Eye steaks have been consumed, the Cuban cigars have been smoked, and the cognac enjoyed, in celebrating months of working and consulting with funders, attorneys, fellow board members, shareholders, what feels like the deal of the century, trouble is lurking on the path forward if you are not careful. You need to define the operational boundaries early-on to avoid chaos later on.

A recent experience brought back memories of the movie “The Devil’s Advocate.” It depicts how easy it is to get influenced without you even realizing it. If you have not watched it, now may be a good time to do so.

Be careful. Attached to asset-based lending comes hidden requirements and operational doctrines that lead to de facto control, notwithstanding that the asset-based lender is neither an equity investor nor a company director. That de facto control, if not managed properly will tax your finance and operational teams. Before you know it you, your company and staff are running around like chickens without heads, scrambling to meet endless “asks” and demands. Without a doubt, assembling and resending the same information over and over. Welcome! You are now in the land of chaos and your business suffers as every one in the company is now working 24/7 to meet funder information demands on top of other crtical work.

Connect with me to help and assist you in safeguarding your business from future challenges attached to asset-based lending.