Many factors are at work at the same time from different economic perspectives shaping the outlook for oil and energy markets in 2022. The world is more uncertain, climate change transitioning serving up its own realistic challenges, geopolitical tensions, as seen many years past, are at the order of the day, and the low investment in oil and gas, since 2015, is ushering in a period of high and rising oil prices. It is the overriding key factor driving the price, of not only oil, but key commodities too.

Commodities require vast amounts of cheap and reliable oil and energy resources to process and distribute it. Economics 101 teaches us that where demand exceeds the sustainable supply, the price will rise.

This is exactly what set in during April 2020 when a new commodity super cycle came into existence. The demand for Renewable Energy (RE) components drive the demand for critical minerals. Even such critical minerals need oil to process and transport them. To add insult to injury, there are not enough critical minerals easily and readily accessible to support an aggressive sustainable transition to RE.

Energy shortages fuel rising costs in all areas of the global economy. All peoples of the world will feel the bite attached to what is now quickly becoming concerns over energy and food insecurity. The world has lost sight of reality when aggressive climate change policies ramped up to support an ideology in which the effects are not fully being understood nor quantified.

An obsession with ideology, which is driven by consensus science, is leading to creating more uncertainty and more complex problems to solve as we move towards achieving the Cop26 and 2050 net-zero goals.

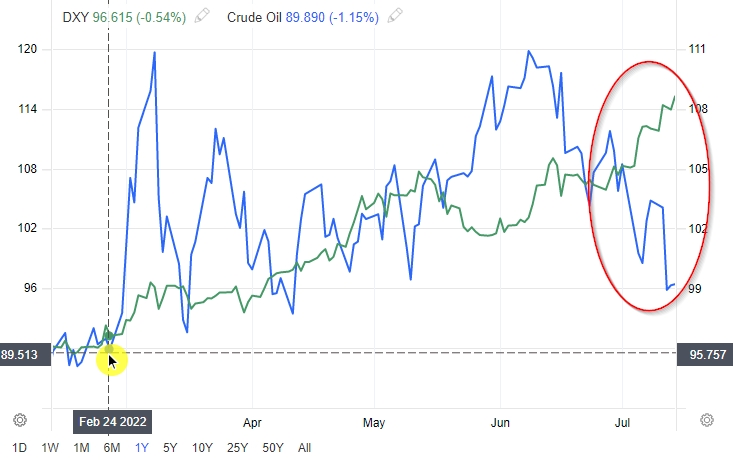

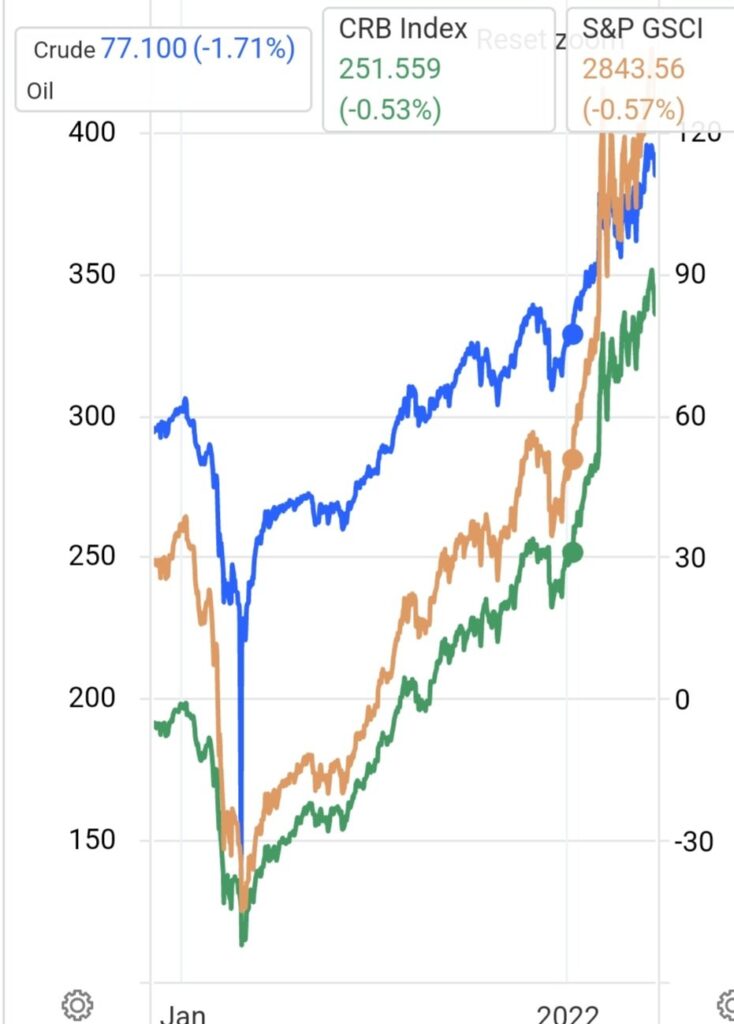

At the time of writing, US Dollar strength (Dollar Strength) was not evident. Since writing in 2021, about the current commodity super cycle (that formed in April 2020), the million-dollar question remained then what Dollar Strength could do. We have seen both commodities (CRB Index, S&P GSCI Index) and crude oil pulling back. Mainly driven by Dollar Strength amid the sharp rise in US interest rates combined with the US Dollar as safe-haven status. With that, almost all short-dated yields in the USA are now above the long-term US government 10-year yield.

source: Trading Economics

source: Trading Economics

What we observe is contributing to the oil-financial market and the oil-physical market moving sharply out of alignment. The fundamentals, as I discuss and point out to them below, remain valid. The reality is the world is short oil and many other key energy commodities. Goldman Sachs, and specifically Jeff Currie, leading Commodity Economist, points out the imbalances that are prevailing in energy markets with the expectation that it will take a long time for supply and demand to be fully back in equilibrium.

Seeking Alpha writes: “Commodities took a dip in June, despite strong performance in the first half of 2022. We believe the outlook for shortened supply is unchanged and may keep commodities in a long-term bull market.”

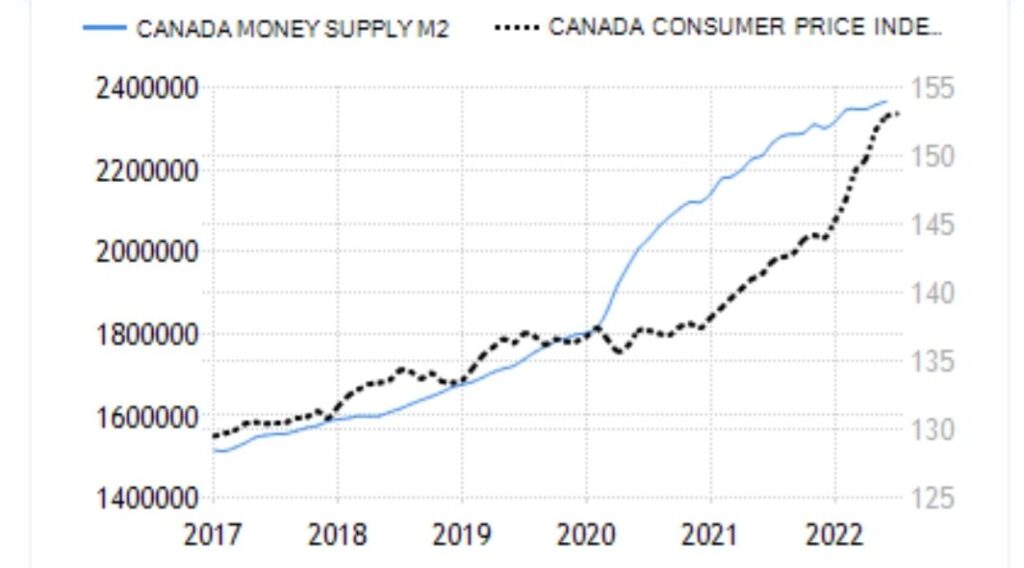

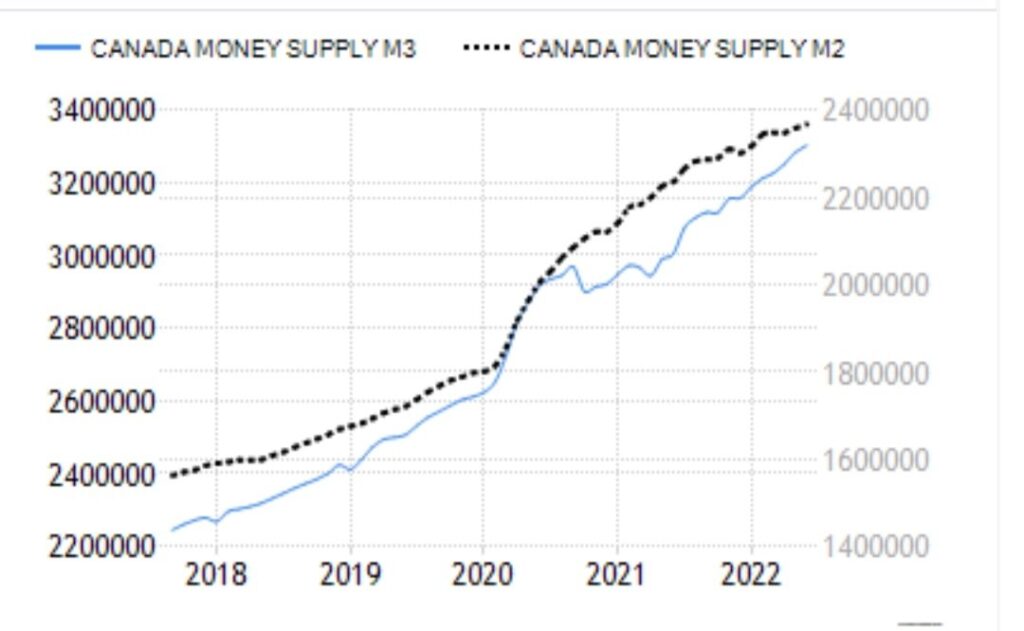

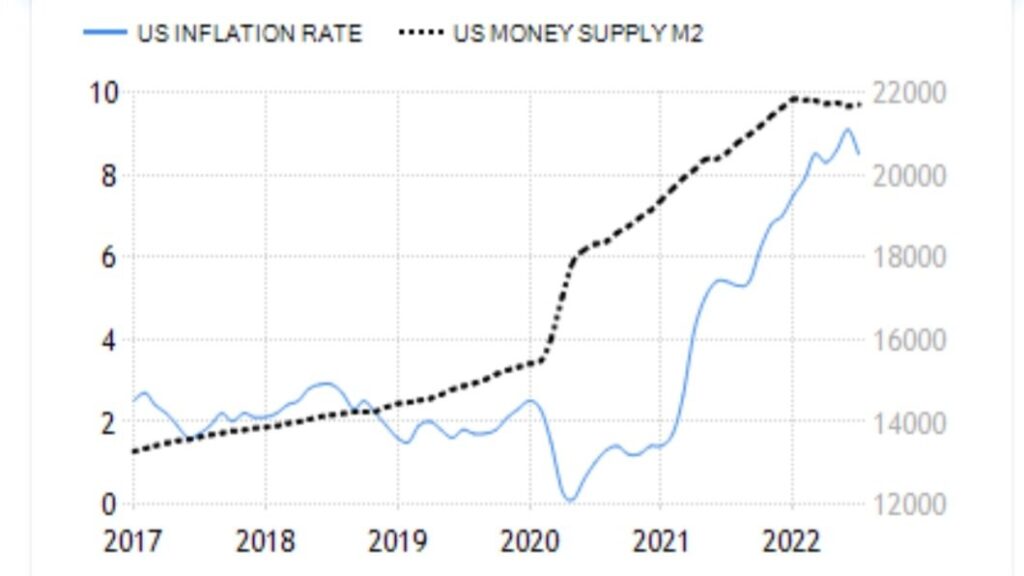

The role that a lack of-, or weak productivity plays in the inflation-, Central Bank- and Money Supply equation is being ignored, and hugely under-valued.

We find ourselves in an era of slack productivity. Reduced productivity combined with the Covid-19 government funded programs have become a toxic mix that adds to the current economic environment of high inflation amid (in order of driver):

Weak climate change policy reducing investment in oil and gas since 2015;

Rise in commodity prices since April 2020 amid aggressive growth in demand for commodities required to produce RE component parts (lithium for batteries) against a shortage of critical minerals (or under developed critical minerals mining cited by the International Energy Agency in 2021 research papers);

Rise in oil prices driven by the aforementioned points amid large imbalances between oil demand and real oil supply.

Source: Trading Economics

Sharp rise in inflation and money supply (which Central Banks deny, yet numbers don’t lie) stemming from the rise in oil & natural gas prices, and money printing by federal governments, all stemming from aforementioned;

“Global bond markets have suffered unprecedented losses since last year.”

It was evident then already, by mid-2021 that all the central bank talk, about inflation being transitory, was merely tactics to suppress rising bond yields.

Bond markets are predictors of what to expect going forward.

In early 2021 bond yields started to rise fueled by inflation concerns. Those concerns were valid because:

Commodity prices started rising during 2020. A new commodity supercycle started to form in April 2020;

Commodities’ rise is fueled by demand for core commodities used in renewable energy. This demand in return is fueled by policies backing the “green new deal” and climate change hysteria:

Demand for commodities drives the thirst for oil and gas. Commodities cannot be processed without the use of oil;

Increased demand for oil causes the oil price to rise. Oil and gas are major input costs in all goods and services being consumed, this transportation costs rises

Inflation is also fueled by massive govt spending on Covid-19 support programs. On top of that, the world is in a huge debt position considering all debt, both government and private sector debt, that exceeds ~500% of global GDP. Global government debt alone accounts for ~226% of global GDP.

Adding fuel to fire stemming from Quantitative Easying (QE) impacting money supply.

Looking back now, who in their right minds could give thought, weighing everything together, that inflation in 2021 was transitory? The central bank elites with impressive PhDs got it wrong. Are we on our way to stagflation? The probability for that is increasing.

O, and it’s ridiculous to refer to the inflation landscape as “Putin-flation”. It is not. World events of late merely added to an already unfolding inflation story.

I think it’s been a big mistake, quite frankly,” Mr. Biden said Tuesday on the sidelines of the summit. “The rest of the world is going to look to China and say, what value add are they providing? They’ve lost an ability to influence people around the world and all the people here.”He said he felt the same way about Russia. “Literally, the tundra is burning,” Mr. Biden said of Russian President Vladimir Putin. “He has serious climate problems and he is mum on his willingness to do anything.

The truth and reality is, China gets it. Without fossil fuels, it’s much harder, costly, and more challenging to transition to net-zero.

China seems to have adopted a two-pronged strategy around duality. Keep on relying on fossil fuels whilst developing Renewable Energy. It’s a phased approach.

China is rated high on the “food chain” concerning electric vehicle (EV) developments. Yet, it still has to set a legislative date when the country will ban the sale of Internal Combustion Engines (ICE) in the future.

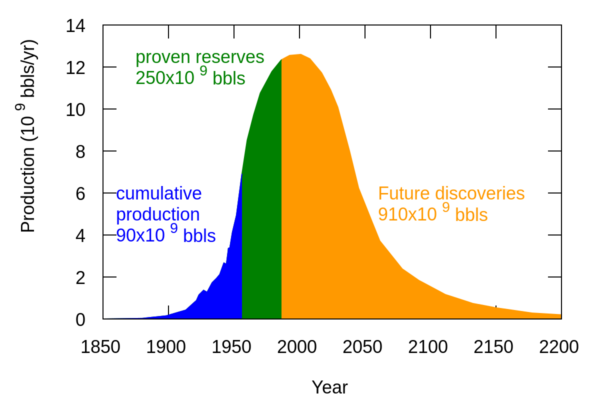

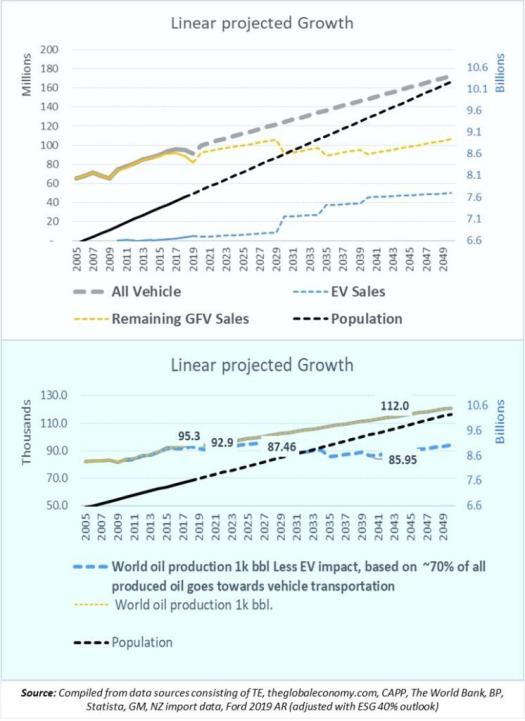

Excluding the impact that China may have on global oil demand, the graphic below depicts what the reduction in the demand for oil may look like considering EV legislated cut over future dates. The analysis includes the bold ambitions of Ford and General Motors announced earlier in 2021.

The demand for oil will not disappear instantly. Mankind is the “Siamese Twin” of energy. Without energy, poverty eradication efforts will fail. Without oil, the quality of life will be substantially lower.

A very big part of what is being missed, in all climate change adaption and transition policy and discussion, is the undeniable fact that what we are looking to transition to, being RE, has many obstacles still to be solved around storage, reliability, and replacing baseload. Solving those are more important compared to the effort being invested in sizing up Green House Gas emissions reduction targets.

On top of that, electric grids require massive expansion and capital to expand capacity to feed and support the increase in demand stemming from charging needs. That’s not the issue but rather a consequence.

What’s different with this energy transition compared to when society transitioned from horse and carriage to the ICE, was that what we transitioned to was cheap and in unlimited supply.

In comparison, RE energy is free from the sun and wind. However when the sun shines and when the wind blows. The current global energy crisis, yes it’s driven mainly by low investment in fossil fuels since 2015, and compounded by lower wind occurrence to drive reliance on RE wind.

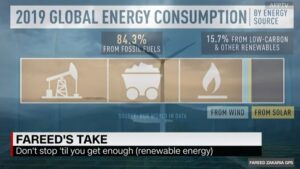

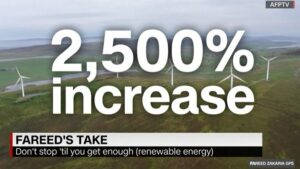

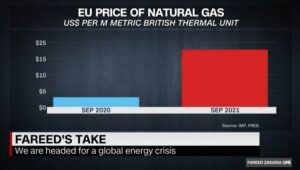

CNN’s Fareed Zakaria sums it nicely. We need an energy transition strategy. Even if the world can reduce GHG emissions the reality is the world still depends on ~84% of its energy needs forthcoming from fossil fuels.

The question is how much RE is required to fully replace fossil fuels? RE investment and expansion still have a long way to go.

We are undeniably in a compounding energy crisis. It’s merely the beginning gauging the recent rise in electricity production costs in the US and Europe.

Put the climate hysteria to the side and develop policies and strategy that embraces duality as the world transitions to RE.

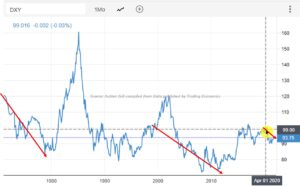

In another post of the current commodity supercycle unfolding I made reference to commodity supercycles also being supported by accompanying dollar weakness.

What are we looking at and what are we observing:

The US Dollar (USD) as measured by the DXY Index vs. the Commodity Research Buro (CRB) Index

We compare the start of the commodity supercycle of 2002 to 2011, and more specifically, the behavior of USD weakness and commodity strength shortly after the onset of the supercycle, to the behavior today (far right) of the onset of the current commodity supercycle (that started in April 2020), and more specifically the behavior of USD weakness and commodity strength shortly after the onset of the supercycle;

The inverse relationship between USD weakness and commodity strengths was when the last commodity supercycle gained momentum around 2004. We are perhaps not there yet in the current cycle; and

The current USD weakness is less inversely correlated with the CRB index. The CRB Index performance at the start of the current commodity supercycle is much more aggressive in relation and is at a steeper inclination compared to the start of the commodity supercycle of 2002 to 2011.

Will the premise hold that a commodity supercycle is also partly driven by USD weakness? What is different this time around?:

When the commodity supercycle started in 2002 the world was:

flush in oil to support increased manufacturing and shipping;

Renewable Energy (RE) was mainly talked about with less strongly articulated RE policies; and

China was the main driver of growth experiencing economic growth above ~10% constant double digits. China also became the “world’s factory”

The start of the current commodity cycle:

lacks the benefit of sufficient investment in oil and gas;

RE and energy transition is contributing to an energy crisis;

Vast under investment in oil and gas since 2015 driven by climate activism

China’s economy is showing signs of slow growth;

RE and Electronic Vehicle legislated start dates (dates that Internal Combustion Engines end to be sold in countries) driven the energy transition to green with a specific demand for core commodities (lithium, cobalt, copper) and component parts that are required for the manufacturing of microchips. Microchips are experiencing severe supply chain challenges not expected to be resolved before 2023. What does that do to pivoting to selling more EV’s?;

RE core commodities experiencing demand that exceeds supply; and

Covid19 that contributes to labor shortages and shipping backlogs

I believe the fact that many nations, including the USA, which is also the world’s reserve currency nation, are focused on RE development and energy transition, could see the inverse correlation panning out differently from what we observe from previous commodities supercycles. Would this suggest that the impact on inflation for many nations could be more severe, rising commodity prices combined with relatively less weak USD performance?

Financial Post: Peter Tertzakian: We are witnessing the perils of a disorderly energy transition

Peter Tertzakian: We are witnessing the perils of a disorderly energy transition

Renewables going up is not translating into oil and gas going down

Eugene Van Den Berg, Oct, 2021

From the article above the Financial Post writes:

“Climate crisis plus energy crisis does not equal a good path to net-zero emissions. Policy wonks at the upcoming COP26 conference in Glasgow later this month will have a tough time with this calculus.It’s been a while since the phrase energy crisis has been thrown around. When I hear it, I have déjà vu to the 1970s. We are witnessing the perils of a disorderly transition, the consequence of mismanaged efforts at decarbonizing the world’s energy systems.

And as with the financial crisis of 2008, which spread around the globe because of systemic risk and contagion, the current energy crisis is spreading from Europe to China to Brazil and soon it will start hurting here at home, North America notwithstanding all the Natural Gas and Oil reserves. the last 7-years in Canada are painted with canceled projects all in the support of the climate agenda. Even though Canada has the world’s 3rd largest oil reserves, it means “squad” because the means to carry it to market for Canada and the world to benefit from has been amputated amid the canceled projects. Even if projects are started now it’s too late and will not be completed in time to fend off any energy crisis. It’s ironic, given that the low Green House Gas (GHG) emissions are being recorded by Canada at ~1.6% of the global total. Another astonishing fact is the quick argument that Canada has a very high emission per capita. I’ll write about that in a separate post safe to say that when we talk an=bout “per capita” both sides of the “per capital” coin are important to grasp. Canada is also painted as having a very high emissions intensity per barrel of oil produced. Nothing is further from the truth as Canada’s record compares favorably to the rest of the world. More about that in another post.

Peter Tertzakian, uses a great analogy, in the above article: ” In business, the word ‘transition’ embodies the premise that people replace old products and processes with new. Sales of the latter grow and the former wane. For example, paper map sales go down when GPS unit sales go up.I didn’t stop buying maps, nor took them out of my glove box, until I was convinced GPS was leading me to the right destination and that there was ubiquitous signal coverage wherever I went. Maps may be a trite analogy to oil, but here is the point: Preserving redundancy through a transition offers continuity of a function, security, and a sense of comfort.“

Another way to look at it can be found in history in the late 1800s to early 1950s. The transition from horse and carriage to Internal Combustion Engine (ICE, or car).

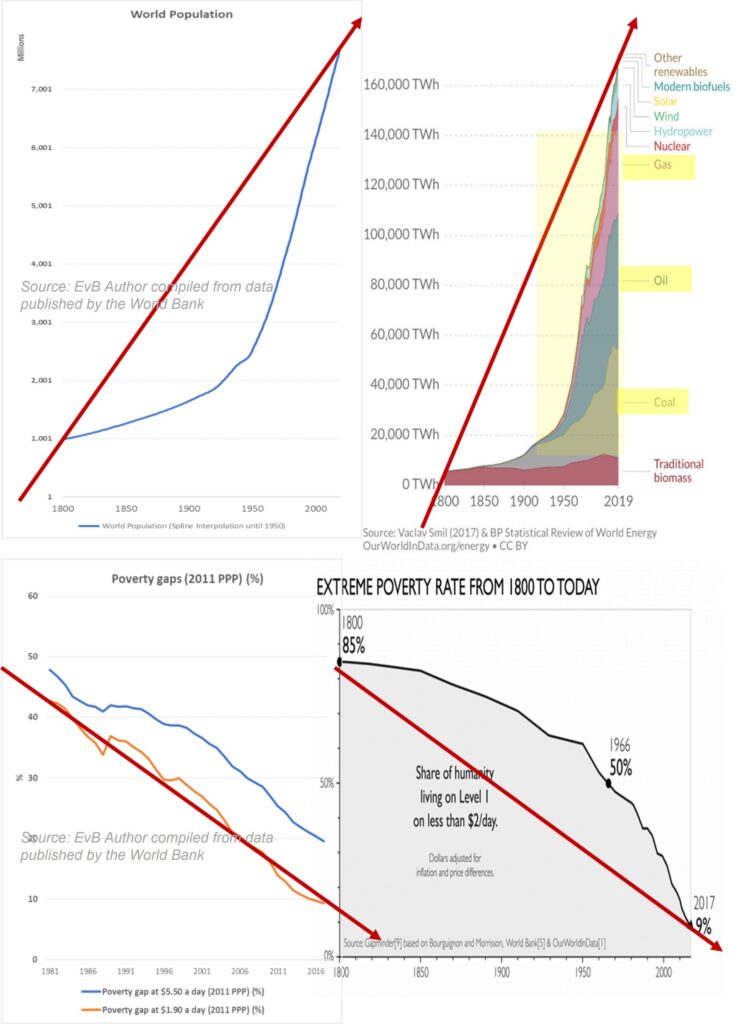

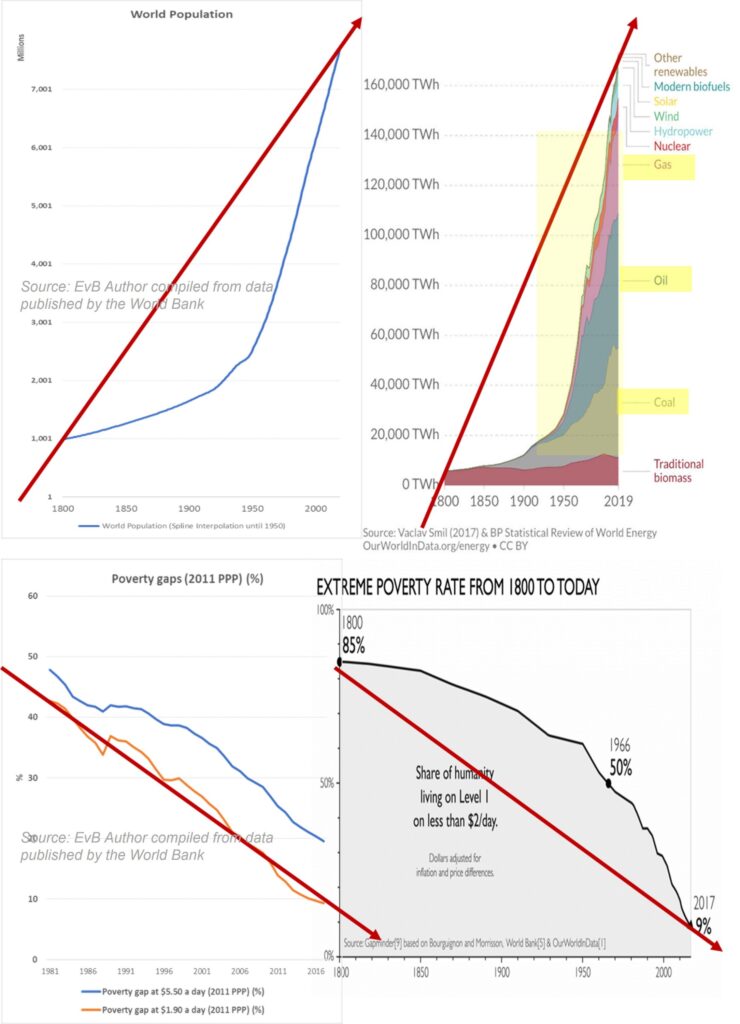

When mankind transitioned from horse-to-car it spanned approx. 50-years. The difference then was, making the transition from one reliable source of transport to another cost-effective source of energy to drive transportation. Businesses like blacksmiths went bust only to be replaced by tire shops and dealer repair shops. The transition took place to an energy source in the abundance of supply, reliable, easy to obtain, and cost-effective. No doubt that fossil fuel drove the enhancement of the quality of life for all on planet earth. Fossil fuels play a key role in poverty eradication too evident when comparing the correlation trend between energy consumption, population growth, and poverty eradication.

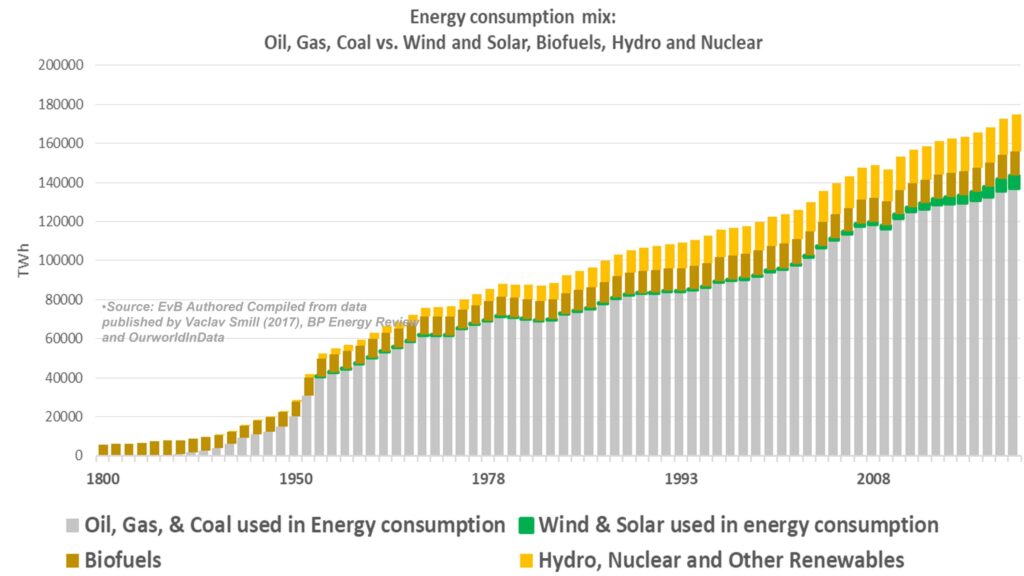

The transition from fossil fuels to Renewable Energy, and specifically wind- and solar power, aims to capture and tap 100% into the unlimited supply of the sun’s energy and the wind’s power. That’s great, free energy resources, who can say no to that. However, the reality is that although win and sun energy exist in an abundance of supply, the methods in capturing and storing it are the challenges that are tripping up making inroads into this behemoth megalodon transition goal. Wind and sun as of now, contribute approx. 17% and 25% of installed capacity. One can ask a valid question about this. If the climate change agenda has been in effect for ~30-years, why is the effectiveness of its contribution to energy consumption low and seems to remain low? What is preventing these forms of energy to capture compounded market share (of utilization NOT generating capacity)?

The world will still be dependant on fossil fuels for the foreseeable future.

As developed nations race towards ESG utopia ideology and cancel old faithful fossil fuels, other countries like Saudi Arabia and Iran welcome the giving of free gifts in terms of global oil market share. The developed world daily is donating market share to these countries on a silver platter. Imagine the cost for course reversal one day at which point it will be too late and we are likely going to repeat 1973 many times over before we land in ESG utopia. For them, it’s “partying like it’s 1999”, never to be repeated again. This, that right there, plays into concerns of future energy security. I get a feeling and a vision of a “MadMax” landscape where the less ethical controls all the oil when we are long still not quite done with oil and gas. We are following ourselves to ignore “duality” as the basis of transition.

Enthusiasm from individual traders is reshaping the market for nuclear fuel that generates a tenth of the world’s electricity and sending uranium-linked stocks higher.

Eugene Van Den Berg, Oct 2021

From the above article:

“Enthusiasm from individual traders is reshaping the market for nuclear fuel that generates a tenth of the world’s electricity and sending uranium-linked stocks higher. After languishing for a decade after the Fukushima disaster led Japan and Germany to close nuclear reactors, spot uranium prices have shot up to $47.10 a pound from $32.25 at the start of August. They remain below their peak of $137 in 2007”

With the current energy crisis and previous Renewable Energy (RE) transition plans to make a “quantum leap” in the short-term, no that’s wrong. It’s actually “trying to take a shortcut on a global scale to chase an ideology, the world has “injured” itself in doing so”. As we learn in school solving the math problem does not work so well trying to take shortcuts. We may get to the wrong answer, and still get marks for the steps shown in solving the Algebra equation. Let that sink in then you may appreciate that the race to “prefect ESG” creates problems that are best avoided.

Germany wanted to cut nuclear and replace it with RE wind and solar. It did not quite work out as planned.

Other countries are running flat out a stampede to instantly move from coal-fired plants to RE wind and solar, having disregard that energy transition will have better outcomes when executed in a structured and organised fashion. Transition from coal to Natural Gas and Nuclear whilst, alongside that, the challenges around RE wind and solar intermittency is scienced to perfection, including solving battery storage and fast charge challenges for Electric Vehicles, will ensure smoother long-term outcomes.

To top it all off, as we transition, all should be engaging in planting trees and replace forests being destroyed in a rehabilitation ratio of [1:10]

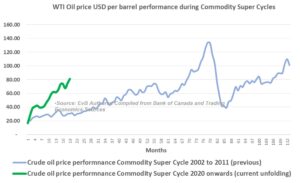

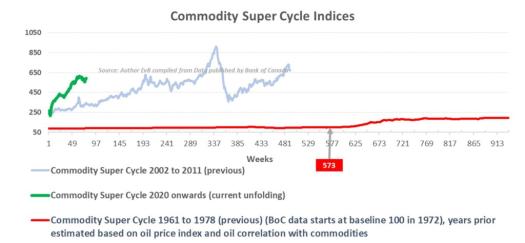

YES!, We are at the start of a Commodity Super Cycle. The previous cycle ran from 2002 until May 2011. Indications reflect that the current cycle began around April 2020, when Covid19 was still building up its first wave. One key aspect supporting commodity supercycles is a weaker dollar. (I reflect on that further down in this post)

Commodity supercycles are interesting. Commodities are important to sustain life and improve the quality of life. Commodities are used in all markets, mined in some, and consumed in other parts of the world. As the energy transition gets underway, the catalysts of the start of the current 2020 supercycle, bring new dynamics to supply and demand. This is fueled by government policy and a shift in investment capital away from traditional fossil fuel energy sources to Renewable Energy (Re) sources.

The world will still be dependant on oil for a long time. Oil is the lubricant that ensures manufacturing processes and industrial machinery, used to produce- and convert commodities into products, runs like clockwork. There does not yet exist an alternative lubricant that is environmentally and emissions friendly – it simply just does not exist no matter how one looks at it, or how hard one is trying (It’s that “Interstellar effect” I refer to). That is one of the factors why there is a strong correlation between the behavior of oil prices and commodity index movements evident from this analysis comparing commodity supercycles and the behavior of oil prices during those same cycles.

Their academic construct is believed to lie in what is referred to as a “Kontradiev Wave” – “A Kondratiev Wave is a long-term economic cycle in commodity prices and other prices, believed to result from technological innovation, that produces a long period of prosperity alternating with economic decline. This theory was founded by Nikolai D. Kondratiev (also spelled “Kondratieff”), an agricultural economist who noticed agricultural commodity and copper prices experienced long-term cycles. Kondratiev believed that these cycles involved periods of evolution and self-correction.”

Deep historic data on commodity supercycles are hard to come by. The main commodity index, The CRB Index (Commodity Research Buro Index) is the most widely used commodity index for measuring performnance. Many Central Banks, like the Bank of Canada, have invested in developing indices and research over the years.

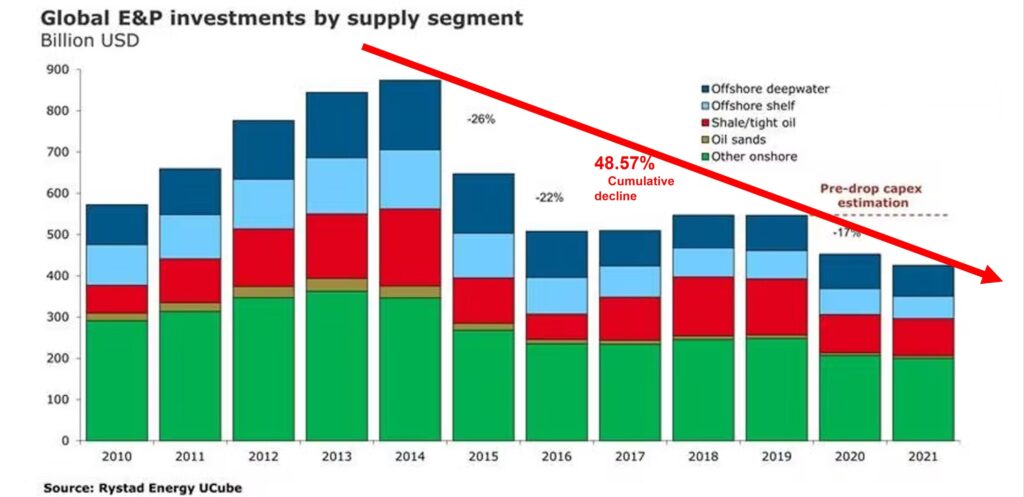

A strong understanding of commodities and how they behave holds implications for planning, policy, and investment of capital. For instance mining projects to build the mining infrastructure to extract commodities (mainly commodities other than agricultural commodities) take years to develop tieing up capital. If the future is uncertain, capital is not invested in projects that would otherwise fulfill expected demand (Economics 101). This is why the world is experiencing an energy crisis starting in 2021.

Over the past few years, anti-fossil fuel activism and government policy promoted to fasten the transition to RE and contributed to capital flight from oil and gas investment to RE and Environmental Social & Governance (ESG) development. To the point that banks and investors publicly announced (and continue to announce, led initially by the European Investment Bank (EIB)) that they no longer will support investment in fossil fuel. Now, and even as acknowledged by the International Energy Agency, based in Paris, earlier in 2021, demand exceeds the supply of oil and gas. This demand imbalance is driven by a number of factors, chiefly, the lack of capital investment since 2015.

How does the current commodity supercycle compare to the performance of the previous two supercycles? The cycle, two cycles back, lasted from 1962 to 1995 (peaked during 1978). The last supercycle lasted from 2002 until recently (peaked in May 2011).

The supercycle during 1962 to 1978 (peak) period was notably a long cycle in comparison to the 2002 to 2011 commodity supercycle. The previous supercycle (2002 to 2011) was driven by the awakening of China, Chinese urbanization, high demand for steel and cars, people migrating to cities for improved quality of life, the world investing capital in China due to ample supply of labor (hence the term “China is the world’s factory”), etc.

The current cycle is much stronger driven by a number of underlying factors working in on each other:

Policies underpinning RE developments;

RE developments demand vast core commodities (copper, lithium, cobalt, aluminum, etc). Electric Vehicles (EV’s) demand more copper than Inter Combustion Engines (ICE) and require more microchips. Microchips too are under severe supply crunch expected only to be elevated in 2023;

RE commodities are experiencing supply chain bottlenecks (and we hardly get out of the RE-shift starting blocks);

Inflation caused by supply chain challenges, consumer demand, and chiefly governments printing vast sums of money to fight Covid19 support programs. Economies too are facing deficits; and

Stampedes of capital shifting from the Real Economy to the Green Economy. That capital drives the demand for new and different types of products and services. It creates a feedback loop into the demand equation for cor commodities and fueling inflation; and

Inflation spirals cause RE energy component parts and other goods and services to rise faster than what can be supplied.

Due to the lack of data prior to 1972, I had to improvise. Given the strong correlation between oil price behavior and commodities’ performance, I constructed an oil price index for that time frame and applied it in reverse onto the commodity data being published by the Bank of Canada.

It’s clear that the supercycle unfolding in 2021 is the strongest in recent memory. I am intrigued by this. I then developed data by comparing the average commodity index reading for each year and compared that to annual population growth. A strong long-term-trend-correlation is observable between population growth and commodities.

That’s correct, as commodities, like energy, sustain life on earth. I recently “coined” the “phrase”, “Mankind is the Siamese Twin of Energy” I’ll expand that to also add “Energy is, in turn, the Siamese Twin that connects Mankind and Commodities”. We end up with a triangular relationship.

It is very important to fully understand the impact of policy and activism supporting the ideology of “RE in an instant”; and its impact on this triangular relationship. The world now is learning a good lesson a hard way risking the exacerbation of energy poverty for many and fueling energy insecurity. It’s the revenge of the “Real Economy” as shared by Bloomberg in a podcast with Jeff Currie from Goldman Sachs driven by under-investment, which in turn is driven by climate activism. (Copy of the transcript)

Are we seeing Us dollar weakness against other currencies that would cement the argument of a full-on commodity supercycle? It’s one aspect one would have to watch carefully. Most commodities are priced in USD, to make them affordable, when the commodity, priced in USD, rises in value one would expect the counter currency-denominated for that specific commodity to appreciate against the USD. In comparison to previous commodity supercycles, the USD depreciated ~5% against a basket of currencies as measured by the US Dollar Index since April 2020, the start of the current commodity supercycle. The CRB index is up ~128% since April 2020 and up ~ 39% since the start of 2021. During the previous commodity supercycle, the USD depreciated approx. 18% against the basket of currencies.

Earlier in 2021, I wrote about inflation, commodities, their connection, etc. I share some of these earlier thoughts given their relevancy to what we are experiencing:

In May 2021

Solar Power’s Decade of Falling Costs Is Thrown Into Reverse - Energy News for the Canadian Oil & Gas Industry | EnergyNow.ca

May 23, 2021 (Bloomberg) A key selling point that made solar energy the fastest-growing power source in the world—rapidly decreasing costs—has hit a speed bump.Solar module prices have risen 18% since the start of the year after falling by 90% over the previous decade. The reversal, fueled by a quad…

“Renewable Energy & Commodities. – Decades of falling costs are reversing” “We are on the cusp of the onset of a Super Commodity Cycle for a number of reasons. Chief of which is driven by the rise in demand- and rise in manufacturing demand for producing RE component parts. Copper, Lithium, Cobalt to mention only a few rose sharply since start of 2021. The thing is ALL commodities are running on steroids. A price reversal of 18% cited in the article, at such an early stage (this is only the beginning) into the rising demand for commodities will crowd out into higher inflation (property investment is your best hedge against inflation, plus Lumber rose ~80%) fueled mainly by RE gvt policies that are behind the demand and commodity price increases. My take: keep a close watch on commodity prices, inflation and bond yields. Get ready for the start of a likely long sustainableSuper Commodity Cycle. We actually need it, I have my front row tickets ready to enjoy the action that is coming. Let’s have a party like it is 1999! #markets #economy #inflation #bonds #interestrates #investing #stocks #tradewar #volatility #market #manufacturing #sustainable #supercommoditycycle #commodities”

In May 2021

IEA: Net-Zero Goal Means No More New Oil And Gas Investment Ever | OilPrice.com

The world doesn’t need any new investments in oil and gas beyond what is already approved if it hopes to achieve net-zero emissions by 2050 according to a new IEA report

“No more oil and gas investment ever.” “Really? and not so fast! And here is “Why” Rising demand for RE component parts is already pushing key commodity prices and demand up (copper, cobalt, lithium, and rare earths). Other commodities too are rising fast. Covid19 bounce back alone could see demand exceeding supply. Taken all together, should we see a Super Commodity Cycle officially taking hold, the thirst for oil (driven by manufacturing demand to process raw materials and goods) will see the oil price and production rising before it may go down as a result of RE policies. Factoring in a likely EV conversion curve (based on mandated government dates to stop selling ICE vehicles), could see annual oil demand fall from ~100m Bbl/d to ~83m Bbl/d by 2050.” #oil #investing #energy #renewableenergy #economy #markets #investing #stocks #economy #interestrates #bankers #oil #growth #market #recession #inflation #bonds #volatility #investments #renewableenergy”

“Not just Covid19 Pent-up demand.” “It’s more, much more! All commodities are up sharply. Inflation will rise. #markets #investing #stocks #economy #interestrates #bankers #oil #growth #market #recession #inflation #bonds #volatility #investments #renewableenergy #commoditysupercycle”

In May 2021:

“Inflation concerns?” “For sure!!” “I throw my hat in with David Laidler who wrote the first theory on inflation. His points align with my post here https://lnkd.in/gbKFpyP about rising oil demand, oil price, PMI and Super Commodity Cycles of which we are seeing some early signs of. Inflation has been too low. Inflation that remains too low chokes natural growth. The cake gets smaller yet more mouths want a piece of a shrinking cake. Too high is as bad as too low. I believe many central bankers will wake up a tad too late. Plus, Fixed income markets are never wrong. So listen to what the bonds are telling us. #markets #investing #stocks #economy #interestrates #bankers #oil #growth #market #recession #inflation #bonds #volatility #investments #renewableenergy”

In May 2021:

IEA sees oil demand recovery outpacing growth in supply

Output from OPEC+ group of producers lagged demand by around by 150,000 barrels per day in the second quarter, IEA said

“Oil prices under-valued?; strong outlook for rising oil price & demand?” “YES!” More reports are forthcoming claiming that demand for oil will likely outstrip supply. This will make many climate activists grind their teeth and fall into depressed panicking mode. There is nothing that can be done about that, it is good, and here is why: 1) We are observing early stages of the start of a Super Commodity Cycle similar to the 2000s until 2011. This in turn is fueled by a sharp rise in commodity prices since the start of 2021 (double-digit price rise in 5-months). The question, will it be sustainable?; 2) Covid19 pent-up demand. Some view it as a short-term to medium-term correction, which makes Central Bankers not overly concerned with inflation, but I will dare to say, I believe they are wrong; 3) Large infrastructure spending plans + “building back better” with a strong focus on “Green” & GHGs reduction strategy will create demand for component parts and manufacturing fueling the thirst for oil 4) PMI readings have moved up into the higher 50s suggesting manufacturing expansion; 5) Fear of rising inflation which is evident in bond yields. Central banks are already behind the inflation curve, driven by deficit spending and MMT. #oil #investing #energy #renewableenergy #economy

In May 2021:

“Inflation”. “Yes”, inflation will rise more than in any time during the past 15 years. The bond markets are pricing for that accordingly and I believe inflation will come back in a meaningful way fueled by:

1) short to medium term Covid19 Pent-up demand 2) RE policy, ESG and sustainable finance supporting RE developments. We are already seeing core commodities used for RE rising sharply. This will fuel increased manufacturing activity. On that PMI readings are stronger too 3) Early signs of a Super Commodity Cycle given the large jump in most commodities across the board with dollar weakness. Inflation will be fueled directly by the above. The increased manufacturing will drive demand for oil, which will cause oil prices to rise again feeding back into the inflation loop because of the crowding out effect attached to oil price rise in general. #oil #energy #renewableenergy #gas #oilandgas #markets #economy #interestrates #dollar #market #investing #investments #stocks #finance #economics #gold #manufacturing #sustainable” “#markets #economy #inflation #bonds #interestrates #investing #stocks #tradewar #volatility #manufacturing #sustainable #supercommoditycycle #commodities #inflation”

In April 2021:

“Inflation and bond yield movements.” “Inflation is rising faster compared to the recent rise in bond yields. If commodity prices continue to rise, expect inflation to rise further. Pend-up Covid19 demand, stemming from lockdowns, too may cause inflation to rise faster going forward. Although BoC kept rates steady, it is reasonable to suspect that BoC may be falling behind the inflation curve, which may not be a good thing considering expectations that government debt will rise further (budget 2021), the cost of servicing that debt too will rise. The question is, what would happen to the CAD_USD exchange rate notwithstanding that it remained pretty steady in broad terms against the USD? If Canadian GDP growth lags that of the US; or if Canada is placed on Credit Rating watch with a negative outlook, exchange rate weakness may start to set in. It will be prudent to raise the BoC rate sooner than later to keep inflation at bay and protect the CAD_USD exchange rate, especially where the energy sector weaknesses (due to a lack of pipelines and hence growth in export earnings otherwise possible) may lead to currency weakness. #economy #inflation #BoC #rates #exchangerate #gdp #economicoutput #economicgrowth #budget21 #federalgovernment #weaknesses #bankofcanadarate #coreinflation”

Why Is the Supply Chain Still So Snarled? We Explain, With a Hot Tub

Utah manufacturer Bullfrog Spas depends on a complicated network to bring materials from across continents and oceans. The pandemic put it out of whack.

Eugene Van Den Berg, Oct 2021

The Wallstreet Journal writes about the interconnection of supply chains, which most take for granted as we only see the end product and have a “sort-of idea” of the input materials.

In this article, although the complex procurement system supporting the manufacturing of hot tubs is used to illustrate it, and there are thousands of similar manufacturers in the world, it is an excellent example of the different processes at work to bring a final product to the consumer. The type of process is not limited to only the manufacturing of hot tubs. All products are supported by procurement and supply chains running effectively.

Supply chains are akin to the oxygen flow in your bloodstream. Constraint oxygen causes multiple problems.

Think back to the 1700 and 1800 small towns: one street, a few businesses along the main street. Supplies were sourced locally on the main borders of the city. Think about the general dealer and local horse smith and iron-works depicted in The Little House on the prairies. Live was simple.

Today, sourcing and procurement are complex. It’s driven by globalization and massive integration. The internet, transport modernization, access to information, online transaction processing, communication technology, etc., played a significant role in shifting procurement from local sources, as it was in the 1800s to thousands of miles away on the other side of the globe today

A question I am asking, is how would prolonged supply chain challenges impact working capital and funds flow for businesses? Can it lead to seizing up working capital because of liquidity constraints brought on by delays? What does that do to interim borrowing, capital management, financial restructuring? What does it do to the recognition of liabilities stemming from pending order fulfillment? All these aspects in their own right causes are crowding out effects, and they all share a single dominator, “unforeseen delay.”.

Daniel Turner writes at The Spectator Big Tech is censoring the climate change debate. Excerpts in italics with my bolds. Wittgenstein wrote that as an ontological and epistemological foundation f…

Eugene Van Den Berg, Oct 2021

Form the source the author writes:

“He who controls the language also controls reality, something that today’s left understands brilliantly, even devilishly. The language around climate change and the green movement is one more area the left wants to control, especially given that trillions of dollars in spending are on the line. Big tech is now doing its part to protect the Green New Deal and radical green ideology from dissenting views. Google and YouTube’s recent announcement that they now prohibit “climate deniers” to monetize their platforms”

What exactly is a Climate Denier? Are you in denial when asking question about feasibility, reality, costs, value for money and returns, affordability, etc.?

The Google and Youtube ban comes into effect in November 2021. The ban will cover ads for – and the monetization of – content that contradicts the “scientific consensus around the existence and causes of climate change”.

To question is not denial. Denial means:

de·ni·al

/dəˈnīəl/

noun

the action of declaring something to be untrue. “she shook her head in denial“

the refusal of something requested or desired. “the denial of insurance to people with certain medical conditions”

The interesting words are: a) “content that contradicts the “scientific consensus”, b) “causes of”.

What happens if there are more evidence out there that reflect on the drivers of global warming not limited to Green House Gas (GHG) emissions only? There are reputable peer-reviewed research undertaken that focuses on all causes. What exactly is scientific consensus? A group of PhD’s that meet and drink tea and shake their heads in agreement with each other? Is scientific evidence not based on fact, hypothesis and proven theories. The boundaries with which science operate today is far different from the time of Einstein. Steve E. Koonin’s“Unsettled” aims to explain the concept around consensus. This book received a lot of criticism. However, one need to maintain an open mind. Another great book “Inconvenient facts, The science that Al Gore doesn’t want you to know”, by Gregory Wrightstone

So by questioning the causes of climate change leading to people being banned, marginalized and de-platformed (seems to be the modern-day in-thing to do as we live in a snowflake and cancel culture) infringes directly on freedoms of expression.

No matter how we look at it ALL SCIENCE matter not only selective science (I am not talking about pseudo science. I am talking about science that can be backed up by fact). In addition to that, without energy live on earth cannot be sustained given the strong data correlations between energy consumption, growth, poverty eradication, improvement in life expectancy all driven by population growth. Are the Climate Activists next going to petition the culling of people given these correlations?

The only way to bring all the pieces together is:

to focus on duality for the interim amid the current energy crisis;

vast effort and money to be invested in solving RE (wind and solar) reliability and battery storage efficiency for Electric Vehicles and RE (wind and solar); and

disconnect the aforementioned from hard emissions reduction targets. solve the conundrum in a piece-meal fashion. Not everything can be solved at once.

There are grave problems with the transition to clean energy power

Eugene Van Den Berg Oct, 2021

From the above article, The Economist writes:

“Next month world leaders will gather at the cop26 summit, saying they mean to set a course for net global carbon emissions to reach zero by 2050. As they prepare to pledge their part in this 30-year endeavour, the first big energy scare of the green era is unfolding before their eyes. Since May the price of a basket of oil, coal and gas has soared by 95%. Britain, the host of the summit, has turned its coal-fired power stations back on, American petrol prices have hit $3 a gallon, blackouts have engulfed China and India, and Vladimir Putin has just reminded Europe that its supply of fuel relies on Russian goodwill.The panic is a reminder that modern life needs abundant energy: without it, bills become unaffordable, homes freeze and businesses stall. The panic has also exposed deeper problems as the world shifts to a cleaner energy system, including inadequate investment in renewables and some transition fossil fuels, rising geopolitical risks and flimsy safety buffers in power markets. Without rapid reforms there will be more energy crises and, perhaps, a popular revolt against climate policies.”

Over the past 30-years or so, Renewable Energy (RE) wind and solar failed to capture sufficiently enough energy marketshare to have stored off the current global energy crisis notwithstanding vast subsidies.

Contributing to the challenges are the demand for RE component parts stemming from critical commodities like Lithium, Copper, Cobalt and many more, that are used in manufacturing such parts. These commodities too experiencing demand that exceeds supply, and the last few years are only the start of a massive drive to accomplish energy transition goals. What will demand and pricing likely look like over the next few years.

Electric Vehicles (EVs) too showing strong growth and demands more copper and microchips than Internal Combustion Engines (ICEs). Microchip supply chains are under strain and so are the supply chains of other RE core commodities.

Rex Murphy: This energy crisis has been 30 years in the making. Why is anyone surprised?

None of the elite bound for the grand climate shindig in Glasgow have to worry about unmeetable energy bills

Eugene Van Den Berg Oct, 2021

The current energy crisis playing out in large parts of the world is driven chiefly by the onset of a commodity supercycle that commenced in April 2020, combined with massive under investment in oil and gas since 2015. Such under investment causes demand for oil and energy commodities to exceed supply.

From the above article, The National Post writes:

“The inevitable collision between 30 years of global warming hyper activism — the howling demonization of available, proven energy resources — and reality, is upon us. There is an atmosphere of semi-panic as many of the countries most committed to “getting off” oil and gas and turning their economies over to wind and sun find winter approaching and they, environmentally virtuous as they are, are wondering if they have enough oil and gas and even coal to get through it.”

Commodities in turn drive the demand for oil. Vast amounts of oil is needed to drive the machinery and industrial equipment used to process such commodities. This cycle compounds increases in inflation.

Having gained the opportunity to study further, in the field of Information Technology, combined with deep international financial experience, established the foundation to rapidly develop diversity in Finance Business Processes spanning 12-years after moving to Canada. Continue reading “Canadian Portfolio”

/cloudfront-us-east-1.images.arcpublishing.com/tgam/VOM42FNERVMIFADAG4BVAEFE6M.JPG)