This energy crisis has helped expose ESG’s shortcomings, and we’re all paying the price

Eugene Van Den Berg, Oct 2021

The Globe and Mail writes:

“About a decade ago, investing on ESG principles went from budding concept to moral crusade. About the same time, it emerged as one of the prime tools to fight climate change. In simple terms, ESG – environmental, social and governance – meant investing responsibly. Grubby, carbon-intensive businesses were, in effect, to be punished unless they moved fast to clean up their acts. If they didn’t, investors and customers of the saintly variety wouldn’t buy their shares or products. Companies that did not wreak planetary destruction in the pursuit of profits were to be rewarded. Out with the “bad,” in with the “good,” even if the latter could never be adequately defined. Were Amazon and Tesla “good” companies because they didn’t dig great gobs of fossil fuels out of the ground? Apparently yes, given their spectacular stock market performances. Never mind that Amazon’s gasoline-powered trucks filled the streets or that Tesla’s global supply chain extended to distinctly ESG-unfriendly cobalt mines in the Democratic Republic of the Congo. What was certain was that oil, gas and coal companies, and most mining companies, suffered the ESG backlash, turning them into market laggards and raising their cost of capital. Their lives were made more miserable by the new ranks of ESG crusaders – among then Mark Carney, Michael Bloomberg, Klaus Schwab (founder of the World Economic Forum) and just about everyone on the United Nations payroll – who promoted the glories and rewards of ESG investing.“

So is Green, after all, genuinely Green? What is this facade costing economies?

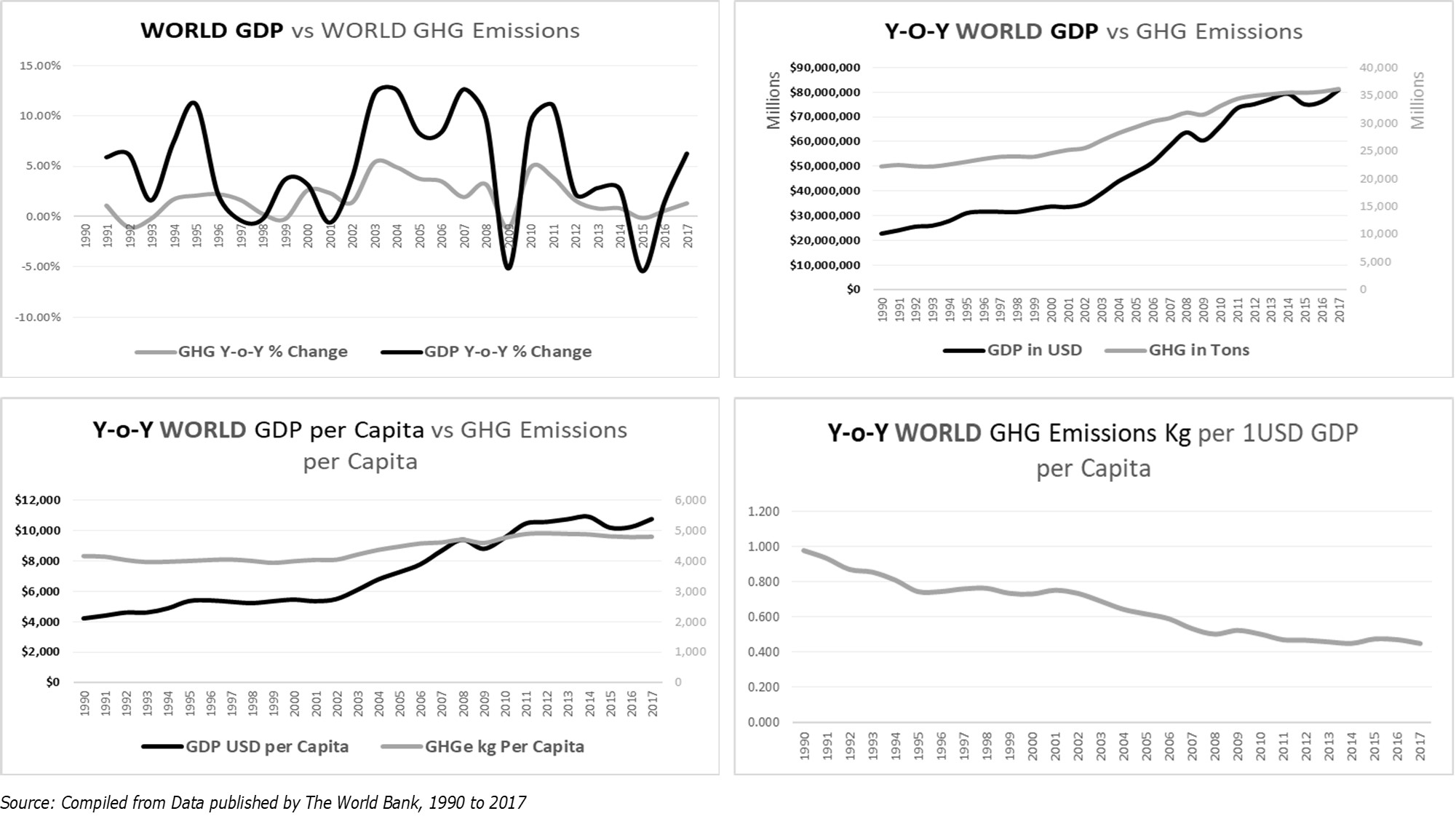

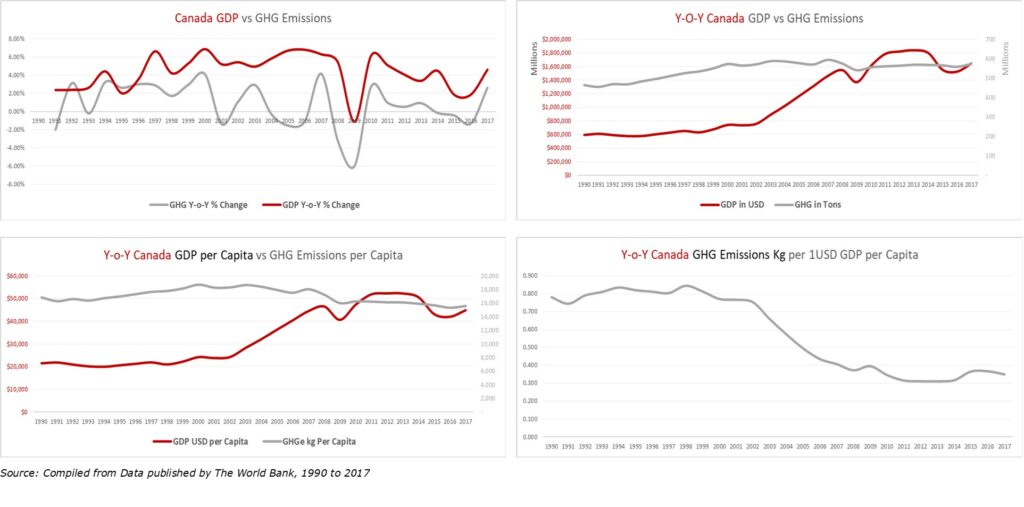

To pivot to Green, and based on calculating emissions, in Kg per 1USD of economic output, globally (when we talk about emissions intensity and per capita emissions, we ought to consider the other side of the same coin, that being, economic output per capita.

You see, there is a strong correlation in all economies between population growth, economic output, and Green House Gas (GHG) emissions. Because of this relationship, one cannot evaluate the one without the other.

In the image below, that relationship, on a global scale, is reflected. The emissions in Kg per 1 USD economic output has steadily declined since the 2000s. That tells us the world is getting better, leveraging technology to reduce emissions for every 1 USD of economic output being generated.

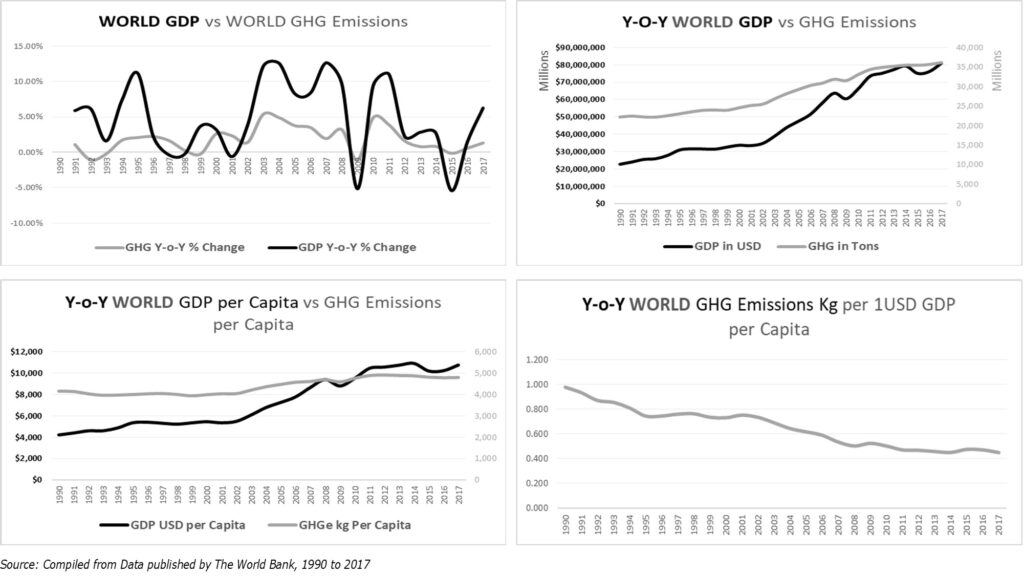

Based on the emissions per Kg per 1 USD of economic output, the Paris 2030 emissions target, which is a 30% reduction lower than the 2005 emissions levels, one can calculate the estimated portion of current-day economic output that has to transform to the “green economy” to meet that target. In other words, what part of the global economic production today needs to be “green” to meet Paris 2030?

It comes down to roughly ~$20 trillion of global GDP., or 26% of global annual GDP output.

This is not the same as the cost of energy transition. In Recent research conducted by The Royal Bank of Canada (RBC), (The $2 Trillion Transition: Canada’s road to Net Zero. RBC estimated the cost of energy transition could amount to ~CAD 2 trillion, the equivalent of approx. a single year’s Canadian GDP output, or roughly ~CAD 60 billion per year. Not a small charge at all.

RBC writes:

“Canada has a math challenge. When it comes to greenhouse gas emissions, Canadians account for a relatively large share of what the world produces. Although we’ve committed over the decades to cut those emissions, we’ve fallen short. We continue to consume conventional energy to cross our vast land and heat our homes, and allow methane to seep into the atmosphere to feed ourselves and much of the planet.”

RBC is wrong about it’s statement that Canada is a large contributor without mentioning the basis on which such false statement is being made. This, from one of Canada’s largest banks. That statement is based on emissions per capita. My above comments show why, when looking at per capita it is important to consider per capita output too. Why ignoring the part of the equation (economic output) that gives rise to emissions per capita? It creates a strong bias to support a political narrative which is dangerous and will cost Canadians dearly in many ways – more energy crises.

Canada has a small population in comparison; Canada is the 2nd largest landmass in the world, Canada is a freezing place. It will consume more energy as goods must travel long distances between the East and Western parts of Canada. It’s approx. 7,366km. That does not even take transportation distances in the Canadian north into account.

Canada is not a significant contributor to GHG emissions. Canada accounts in aggregate for 1.6%, China accounts for 27%, USA accounts for 15%, India accounts for 7%, Russia accounts for 5%, the UK accounts for 1.1%

Canada’s GHG emissions are low, notwithstanding having high demands for energy for the reasons stated. Those reasons cannot be changed. Canada has the benefit of having a boreal forest that covers a large part of Canada. It’s a natural carbon sink. Russia too has a sizeable boreal forest which, given its attributes, contributes to Russia only making up ~5% of the global GHG emissions total.

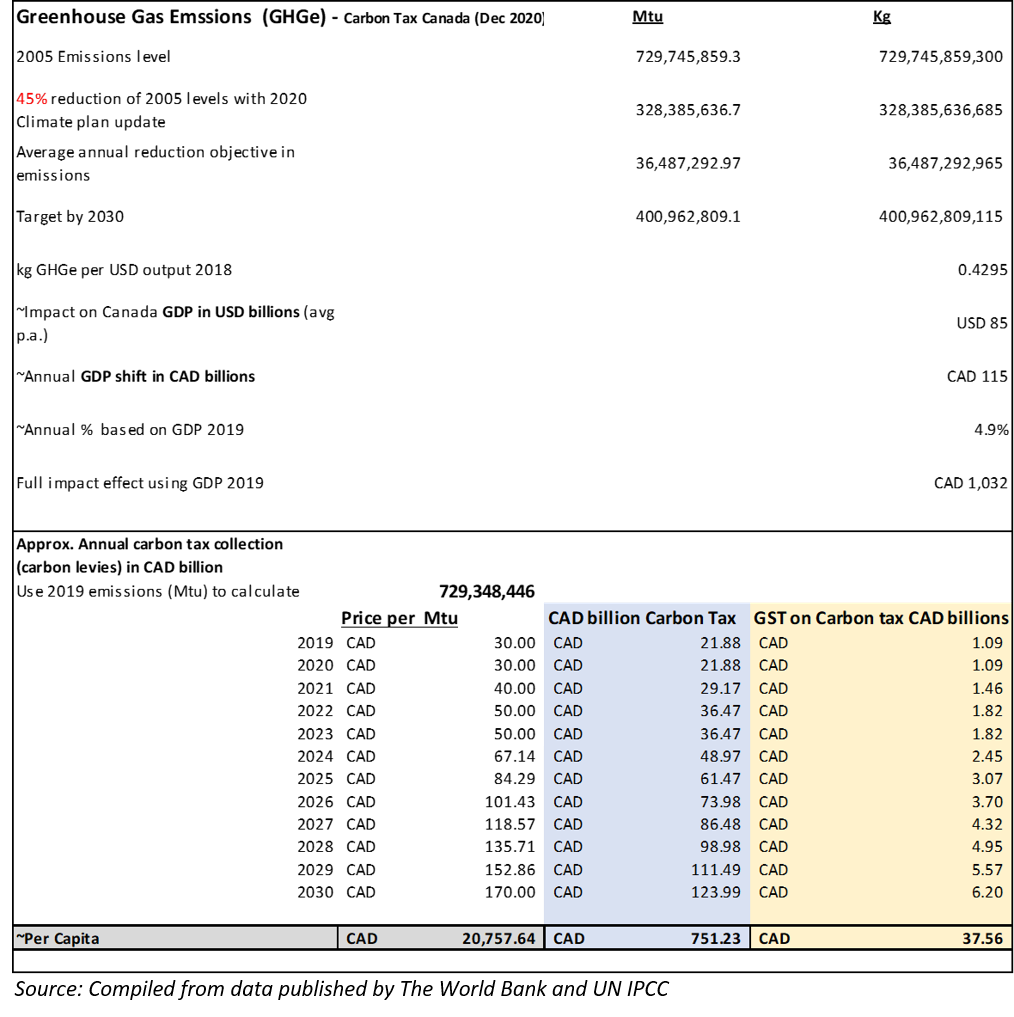

Using the same metrics of what the Canadian economy requires to shift financial output to “green,” to meet the 2030 Paris target (reduce emissions to a level that is 30% less than the 2005 emissions level), Canada needs to shift ~USD 1 trillion cumulative economic output between 2021 and 2030 to meet the Paris 2030 targets. That’s the equivalent of approx. 47% of the current annual GDP.

Stated differently, Canada is to spend ~CAD 60 billion per year to shift ~CAD 115 billion in economic output. Thus the current GDP needs to expand by roughly ~2.8%, to produce the capital required (The CAD 60 billion calculated by RBC) to invest in energy transition efforts.

In other words, the economy needs to grow at approx. 5.8% on an ongoing sustainable basis, year over year for ~10-years to generate the cash to pay for the energy transition. It’s relevant to ask, “how realistic is that given that the fossil fuels industry is the largest contributor to the Canadian economy, but is being marginalized for the past 7 years; Canada is dependant on ~76% of direct trade and exports with the USA. Canada is approx. 10% of the USA in all respects.” – “NOT EASILY DOABLE GIVEN HISTORY!” If Canada cannot diversify its exports and leverage it’s energy to do so; chances are the economy cannot and will not grow at the levels needed to produce the investment capital to make ESG and Net Zero work.

What do we receive in return? The ability to shift CAD 115 billion in economic output to “green”. Spending CAD 60 billion to move CAD 115 billion. It’s an economic ratio of ~52% of what we need to shift to ” green” that we have to spend to go the ~CAD 115.

There are downsides to ESG, the true costs are questionable. RBC suggests it could cost annually ~CAD 40 billion in climate-related disasters if it remains business as usual (BAU). However, just by saying that spending CAD 60 billion to prevent spending CAD 40 billion are wrong for several reasons:

- The investment into energy transition costs doesn’t produce dollar-for-dollar savings. There is no direct correlation. At best, an indirect correlation that has delayed future disaster cost-savings effects;

- There are other means to reduce climate disaster costs. Landuses need to be better managed;

- Humanity does not have proof yet that vast investments will, in fact, generate the targeted emissions education targets.

ESG is coming at a significant cost, a cost that was not foreseen and quantified,

It will take a very long time to reverse the declining investment trend in oil and gas, even if a capital stampede reversal starts now. Oil an has companies are likely “once bitten, twice shy”, ” once marginalused, twice shellfish”. Why should they? It’s more lucrative to ride the wave of tight supply collecting riches.

La Niña may trigger another cold winter, and Russia is not sending enough pipeline gas to Europe. All of these are contributing further to the onset of a commodity supercycle.

RBC further writes:

“This journey will require new approaches to sustainable finance, if we’re to generate the $2 trillion needed to finance the transition. Overall, capital is not in short supply. Investible projects, with reasonable returns, are. What’s needed? An overhaul of industrial regulation and tax policy, and more government backstops, to offset the inherently risky frontier of clean technology, sustainable infrastructure and new consumer products. A lack of consistent and reliable policies continues to impede Canada’s ability to attract the sort of private capital needed to finance the transition.”

If the economy cannot generate ~CAD 2 trillion, lending it through federal government programs will contribute to more debt and deficits. A key catalyst pushing inflation higher over the transition period.

Quite rightly stated by RBC, we need better policies. We need approaches that integrate the path to Net Zero with the transition dependency on fossil fuels while the renewable energy storage, grid demands, and reliability as solved through technology innovations. It’s a dual process, this policy focussing on “Duality.” You honestly don’t need to have a string of Ph.D. letters behind your name to figure this out. All you need is plain old fashioned ” commonsense

Eugene Van Den Berg

Eugene is an accomplished Analyst, Accountant, Controller, CFO, and Corporate Finance expert with many years of diverse finance and accounting experience across different industries and with different companies, including non-for-profits. He is a knowledge- and information worker with a passion to solve complex financial management problems and financial reporting processes. Eugene is passionate about finance and economics. He enjoys blogging about interesting economic aspects of current times. He also enjoys following how politics interjects with finance, economy and statistics. Future academic ambition includes enrolling for a PhD in Economics (for the fun of it!).