Eugene van den Berg, Oct 2021

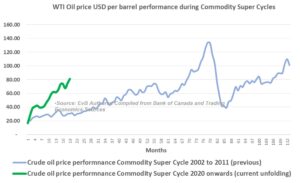

YES!, We are at the start of a Commodity Super Cycle. The previous cycle ran from 2002 until May 2011. Indications reflect that the current cycle began around April 2020, when Covid19 was still building up its first wave. One key aspect supporting commodity supercycles is a weaker dollar. (I reflect on that further down in this post)

Commodity supercycles are interesting. Commodities are important to sustain life and improve the quality of life. Commodities are used in all markets, mined in some, and consumed in other parts of the world. As the energy transition gets underway, the catalysts of the start of the current 2020 supercycle, bring new dynamics to supply and demand. This is fueled by government policy and a shift in investment capital away from traditional fossil fuel energy sources to Renewable Energy (Re) sources.

The world will still be dependant on oil for a long time. Oil is the lubricant that ensures manufacturing processes and industrial machinery, used to produce- and convert commodities into products, runs like clockwork. There does not yet exist an alternative lubricant that is environmentally and emissions friendly – it simply just does not exist no matter how one looks at it, or how hard one is trying (It’s that “Interstellar effect” I refer to). That is one of the factors why there is a strong correlation between the behavior of oil prices and commodity index movements evident from this analysis comparing commodity supercycles and the behavior of oil prices during those same cycles.

Their academic construct is believed to lie in what is referred to as a “Kontradiev Wave” – “A Kondratiev Wave is a long-term economic cycle in commodity prices and other prices, believed to result from technological innovation, that produces a long period of prosperity alternating with economic decline. This theory was founded by Nikolai D. Kondratiev (also spelled “Kondratieff”), an agricultural economist who noticed agricultural commodity and copper prices experienced long-term cycles. Kondratiev believed that these cycles involved periods of evolution and self-correction.”

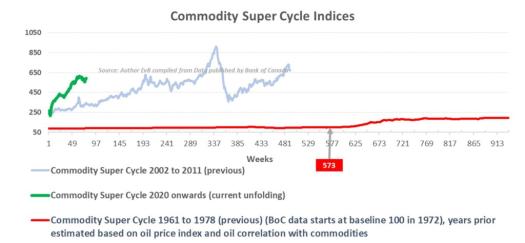

Deep historic data on commodity supercycles are hard to come by. The main commodity index, The CRB Index (Commodity Research Buro Index) is the most widely used commodity index for measuring performnance. Many Central Banks, like the Bank of Canada, have invested in developing indices and research over the years.

A strong understanding of commodities and how they behave holds implications for planning, policy, and investment of capital. For instance mining projects to build the mining infrastructure to extract commodities (mainly commodities other than agricultural commodities) take years to develop tieing up capital. If the future is uncertain, capital is not invested in projects that would otherwise fulfill expected demand (Economics 101). This is why the world is experiencing an energy crisis starting in 2021.

Over the past few years, anti-fossil fuel activism and government policy promoted to fasten the transition to RE and contributed to capital flight from oil and gas investment to RE and Environmental Social & Governance (ESG) development. To the point that banks and investors publicly announced (and continue to announce, led initially by the European Investment Bank (EIB)) that they no longer will support investment in fossil fuel. Now, and even as acknowledged by the International Energy Agency, based in Paris, earlier in 2021, demand exceeds the supply of oil and gas. This demand imbalance is driven by a number of factors, chiefly, the lack of capital investment since 2015.

How does the current commodity supercycle compare to the performance of the previous two supercycles? The cycle, two cycles back, lasted from 1962 to 1995 (peaked during 1978). The last supercycle lasted from 2002 until recently (peaked in May 2011).

The supercycle during 1962 to 1978 (peak) period was notably a long cycle in comparison to the 2002 to 2011 commodity supercycle. The previous supercycle (2002 to 2011) was driven by the awakening of China, Chinese urbanization, high demand for steel and cars, people migrating to cities for improved quality of life, the world investing capital in China due to ample supply of labor (hence the term “China is the world’s factory”), etc.

The current cycle is much stronger driven by a number of underlying factors working in on each other:

-

- Policies underpinning RE developments;

- RE developments demand vast core commodities (copper, lithium, cobalt, aluminum, etc). Electric Vehicles (EV’s) demand more copper than Inter Combustion Engines (ICE) and require more microchips. Microchips too are under severe supply crunch expected only to be elevated in 2023;

- RE commodities are experiencing supply chain bottlenecks (and we hardly get out of the RE-shift starting blocks);

- Inflation caused by supply chain challenges, consumer demand, and chiefly governments printing vast sums of money to fight Covid19 support programs. Economies too are facing deficits; and

- Stampedes of capital shifting from the Real Economy to the Green Economy. That capital drives the demand for new and different types of products and services. It creates a feedback loop into the demand equation for cor commodities and fueling inflation; and

- Inflation spirals cause RE energy component parts and other goods and services to rise faster than what can be supplied.

Due to the lack of data prior to 1972, I had to improvise. Given the strong correlation between oil price behavior and commodities’ performance, I constructed an oil price index for that time frame and applied it in reverse onto the commodity data being published by the Bank of Canada.

It’s clear that the supercycle unfolding in 2021 is the strongest in recent memory. I am intrigued by this. I then developed data by comparing the average commodity index reading for each year and compared that to annual population growth. A strong long-term-trend-correlation is observable between population growth and commodities.

That’s correct, as commodities, like energy, sustain life on earth. I recently “coined” the “phrase”, “Mankind is the Siamese Twin of Energy” I’ll expand that to also add “Energy is, in turn, the Siamese Twin that connects Mankind and Commodities”. We end up with a triangular relationship.

It is very important to fully understand the impact of policy and activism supporting the ideology of “RE in an instant”; and its impact on this triangular relationship. The world now is learning a good lesson a hard way risking the exacerbation of energy poverty for many and fueling energy insecurity. It’s the revenge of the “Real Economy” as shared by Bloomberg in a podcast with Jeff Currie from Goldman Sachs driven by under-investment, which in turn is driven by climate activism. (Copy of the transcript)

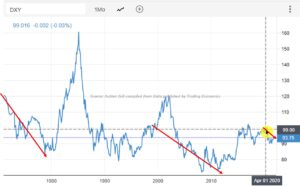

Are we seeing Us dollar weakness against other currencies that would cement the argument of a full-on commodity supercycle? It’s one aspect one would have to watch carefully. Most commodities are priced in USD, to make them affordable, when the commodity, priced in USD, rises in value one would expect the counter currency-denominated for that specific commodity to appreciate against the USD. In comparison to previous commodity supercycles, the USD depreciated ~5% against a basket of currencies as measured by the US Dollar Index since April 2020, the start of the current commodity supercycle. The CRB index is up ~128% since April 2020 and up ~ 39% since the start of 2021. During the previous commodity supercycle, the USD depreciated approx. 18% against the basket of currencies.

Earlier in 2021, I wrote about inflation, commodities, their connection, etc. I share some of these earlier thoughts given their relevancy to what we are experiencing:

In May 2021

“Renewable Energy & Commodities. – Decades of falling costs are reversing”

“We are on the cusp of the onset of a Super Commodity Cycle for a number of reasons. Chief of which is driven by the rise in demand- and rise in manufacturing demand for producing RE component parts. Copper, Lithium, Cobalt to mention only a few rose sharply since start of 2021. The thing is ALL commodities are running on steroids. A price reversal of 18% cited in the article, at such an early stage (this is only the beginning) into the rising demand for commodities will crowd out into higher inflation (property investment is your best hedge against inflation, plus Lumber rose ~80%) fueled mainly by RE gvt policies that are behind the demand and commodity price increases. My take: keep a close watch on commodity prices, inflation and bond yields. Get ready for the start of a likely long sustainable Super Commodity Cycle. We actually need it, I have my front row tickets ready to enjoy the action that is coming. Let’s have a party like it is 1999!

#markets #economy #inflation #bonds #interestrates #investing #stocks #tradewar #volatility #market #manufacturing #sustainable #supercommoditycycle #commodities”

In May 2021

“No more oil and gas investment ever.”

“Really? and not so fast! And here is “Why”

Rising demand for RE component parts is already pushing key commodity prices and demand up (copper, cobalt, lithium, and rare earths). Other commodities too are rising fast. Covid19 bounce back alone could see demand exceeding supply. Taken all together, should we see a Super Commodity Cycle officially taking hold, the thirst for oil (driven by manufacturing demand to process raw materials and goods) will see the oil price and production rising before it may go down as a result of RE policies. Factoring in a likely EV conversion curve (based on mandated government dates to stop selling ICE vehicles), could see annual oil demand fall from ~100m Bbl/d to ~83m Bbl/d by 2050.”

#oil #investing #energy #renewableenergy #economy

#markets #investing #stocks #economy #interestrates #bankers #oil #growth #market #recession #inflation #bonds #volatility #investments #renewableenergy”

In May 2021:

https://www.cbc.ca/news/canada/edmonton/canadian-farmers-commodity-prices-boom-1.6029375

“Not just Covid19 Pent-up demand.”

“It’s more, much more!

All commodities are up sharply. Inflation will rise.

#markets #investing #stocks #economy #interestrates #bankers #oil #growth #market #recession #inflation #bonds #volatility #investments #renewableenergy #commoditysupercycle”

In May 2021:

“Inflation concerns?”

“For sure!!”

“I throw my hat in with David Laidler who wrote the first theory on inflation. His points align with my post here https://lnkd.in/gbKFpyP about rising oil demand, oil price, PMI and Super Commodity Cycles of which we are seeing some early signs of. Inflation has been too low. Inflation that remains too low chokes natural growth. The cake gets smaller yet more mouths want a piece of a shrinking cake. Too high is as bad as too low. I believe many central bankers will wake up a tad too late. Plus, Fixed income markets are never wrong. So listen to what the bonds are telling us.

#markets #investing #stocks #economy #interestrates #bankers #oil #growth #market #recession #inflation #bonds #volatility #investments #renewableenergy”

In May 2021:

/cloudfront-us-east-1.images.arcpublishing.com/tgam/VOM42FNERVMIFADAG4BVAEFE6M.JPG)

“Oil prices under-valued?; strong outlook for rising oil price & demand?”

“YES!”

More reports are forthcoming claiming that demand for oil will likely outstrip supply. This will make many climate activists grind their teeth and fall into depressed panicking mode. There is nothing that can be done about that, it is good, and here is why:

1) We are observing early stages of the start of a Super Commodity Cycle similar to the 2000s until 2011. This in turn is fueled by a sharp rise in commodity prices since the start of 2021 (double-digit price rise in 5-months). The question, will it be sustainable?;

2) Covid19 pent-up demand. Some view it as a short-term to medium-term correction, which makes Central Bankers not overly concerned with inflation, but I will dare to say, I believe they are wrong;

3) Large infrastructure spending plans + “building back better” with a strong focus on “Green” & GHGs reduction strategy will create demand for component parts and manufacturing fueling the thirst for oil

4) PMI readings have moved up into the higher 50s suggesting manufacturing expansion;

5) Fear of rising inflation which is evident in bond yields. Central banks are already behind the inflation curve, driven by deficit spending and MMT.

#oil #investing #energy #renewableenergy #economy

In May 2021:

“Inflation”.

“Yes”, inflation will rise more than in any time during the past 15 years. The bond markets are pricing for that accordingly and I believe inflation will come back in a meaningful way fueled by:

1) short to medium term Covid19 Pent-up demand

2) RE policy, ESG and sustainable finance supporting RE developments. We are already seeing core commodities used for RE rising sharply. This will fuel increased manufacturing activity. On that PMI readings are stronger too

3) Early signs of a Super Commodity Cycle given the large jump in most commodities across the board with dollar weakness.

Inflation will be fueled directly by the above. The increased manufacturing will drive demand for oil, which will cause oil prices to rise again feeding back into the inflation loop because of the crowding out effect attached to oil price rise in general.

#oil #energy #renewableenergy #gas #oilandgas #markets #economy #interestrates #dollar #market #investing #investments #stocks #finance #economics #gold #manufacturing #sustainable” “#markets #economy #inflation #bonds #interestrates #investing #stocks #tradewar #volatility #manufacturing #sustainable #supercommoditycycle #commodities #inflation”

In April 2021:

“Inflation and bond yield movements.”

“Inflation is rising faster compared to the recent rise in bond yields. If commodity prices continue to rise, expect inflation to rise further. Pend-up Covid19 demand, stemming from lockdowns, too may cause inflation to rise faster going forward. Although BoC kept rates steady, it is reasonable to suspect that BoC may be falling behind the inflation curve, which may not be a good thing considering expectations that government debt will rise further (budget 2021), the cost of servicing that debt too will rise. The question is, what would happen to the CAD_USD exchange rate notwithstanding that it remained pretty steady in broad terms against the USD? If Canadian GDP growth lags that of the US; or if Canada is placed on Credit Rating watch with a negative outlook, exchange rate weakness may start to set in. It will be prudent to raise the BoC rate sooner than later to keep inflation at bay and protect the CAD_USD exchange rate, especially where the energy sector weaknesses (due to a lack of pipelines and hence growth in export earnings otherwise possible) may lead to currency weakness.

#economy #inflation #BoC #rates #exchangerate #gdp #economicoutput #economicgrowth #budget21 #federalgovernment #weaknesses #bankofcanadarate #coreinflation”

Eugene Van Den Berg

Eugene is an accomplished Analyst, Accountant, Controller, CFO, and Corporate Finance expert with many years of diverse finance and accounting experience across different industries and with different companies, including non-for-profits. He is a knowledge- and information worker with a passion to solve complex financial management problems and financial reporting processes. Eugene is passionate about finance and economics. He enjoys blogging about interesting economic aspects of current times. He also enjoys following how politics interjects with finance, economy and statistics. Future academic ambition includes enrolling for a PhD in Economics (for the fun of it!).