Many factors are at work at the same time from different economic perspectives shaping the outlook for oil and energy markets in 2022. The world is more uncertain, climate change transitioning serving up its own realistic challenges, geopolitical tensions, as seen many years past, are at the order of the day, and the low investment in oil and gas, since 2015, is ushering in a period of high and rising oil prices. It is the overriding key factor driving the price, of not only oil, but key commodities too.

Commodities require vast amounts of cheap and reliable oil and energy resources to process and distribute it. Economics 101 teaches us that where demand exceeds the sustainable supply, the price will rise.

This is exactly what set in during April 2020 when a new commodity super cycle came into existence. The demand for Renewable Energy (RE) components drive the demand for critical minerals. Even such critical minerals need oil to process and transport them. To add insult to injury, there are not enough critical minerals easily and readily accessible to support an aggressive sustainable transition to RE.

Energy shortages fuel rising costs in all areas of the global economy. All peoples of the world will feel the bite attached to what is now quickly becoming concerns over energy and food insecurity. The world has lost sight of reality when aggressive climate change policies ramped up to support an ideology in which the effects are not fully being understood nor quantified.

An obsession with ideology, which is driven by consensus science, is leading to creating more uncertainty and more complex problems to solve as we move towards achieving the Cop26 and 2050 net-zero goals.

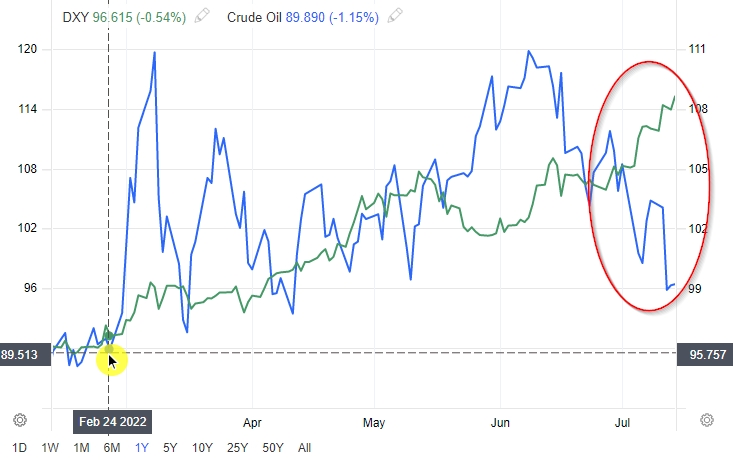

At the time of writing, US Dollar strength (Dollar Strength) was not evident. Since writing in 2021, about the current commodity super cycle (that formed in April 2020), the million-dollar question remained then what Dollar Strength could do. We have seen both commodities (CRB Index, S&P GSCI Index) and crude oil pulling back. Mainly driven by Dollar Strength amid the sharp rise in US interest rates combined with the US Dollar as safe-haven status. With that, almost all short-dated yields in the USA are now above the long-term US government 10-year yield.

source: Trading Economics

source: Trading Economics

What we observe is contributing to the oil-financial market and the oil-physical market moving sharply out of alignment. The fundamentals, as I discuss and point out to them below, remain valid. The reality is the world is short oil and many other key energy commodities. Goldman Sachs, and specifically Jeff Currie, leading Commodity Economist, points out the imbalances that are prevailing in energy markets with the expectation that it will take a long time for supply and demand to be fully back in equilibrium.

Seeking Alpha writes: “Commodities took a dip in June, despite strong performance in the first half of 2022. We believe the outlook for shortened supply is unchanged and may keep commodities in a long-term bull market.”

Eugene van den Berg, May 2022 (updated July 2022)

Eugene Van Den Berg

Eugene is an accomplished Analyst, Accountant, Controller, CFO, and Corporate Finance expert with many years of diverse finance and accounting experience across different industries and with different companies, including non-for-profits. He is a knowledge- and information worker with a passion to solve complex financial management problems and financial reporting processes. Eugene is passionate about finance and economics. He enjoys blogging about interesting economic aspects of current times. He also enjoys following how politics interjects with finance, economy and statistics. Future academic ambition includes enrolling for a PhD in Economics (for the fun of it!).